Our monthly property market review is intended to provide background to recent developments in property markets as well as to give an indication of how some key issues could impact in the future.

We are not responsible or authorised to provide advice on investment decisions concerning property, only for the provision of mortgage advice.

February is the best time to put your home on the market, according to research from Rightmove.

The study analysed property listings between 2014 and 2024 (excluding 2020 due to the pandemic). It found that 68.9% of homes put up for sale in February go on to secure a buyer, the highest success rate of any month. January and March followed very closely, with 68.8% of homes listed in these months successfully attracting a buyer. This suggests that the first quarter of the year is an optimum time for sellers.

While February listings see the highest proportion of successful sales, January listings sell the fastest, taking an average of 47 days to find a buyer. Colleen Babcock at Rightmove commented, “Sellers who are yet to act but are considering a 2026 move might consider coming to market soon to take advantage of the increase in home-buyer activity.”

In January, the government launched the Warm Homes Plan, a £15bn investment aimed at upgrading British homes and reducing energy bills.

Key measures in the Warm Homes Plan include a commitment to triple the number of homes with solar energy by 2030 and deliver over 450,000 heat pump installations each year. Also, £2.7bn will be invested into the expanded Boiler Upgrade Scheme, meaning eligible households can apply for a grant to replace their fossil fuel heating system with a heat pump or biomass boiler. Overall, the initiative is expected to create 180,000 new jobs in energy efficiency and clean heating.

Ed Miliband, Secretary of State for Energy Security and Net Zero, said, “this is a landmark plan to make the British people better off, secure our energy independence and tackle the climate crisis.” But some experts are concerned that the cost of implementing the plan will be more than the allocated £15bn.

In January, leading housebuilders met with ministers to discuss planning reforms and the current state of the housing market.

Housing Secretary Steve Reed chaired the roundtable, which was attended by major developers including Vistry, Taylor Wimpey and Barratt Redrow. Discussions focussed on the government’s target to deliver 1.5 million homes, which has been supported by the New Homes Accelerator announced in August 2025. Reed said, “Thanks to our changes to planning laws we’re now seeing the green shoots of recovery – with an 18% increase in work starting on new homes compared to the previous year.”

Industry figures have weighed in on the discussion. Steve Turner at the Home Builders Federation welcomed the progress thus far but called for further action: “With no government-backed scheme in place for the first time in decades, many first-time buyers are locked out of the market, suppressing demand and limiting the ability to increase supply.”

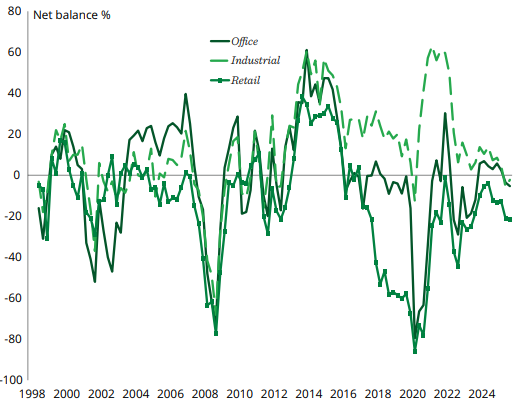

Recent data shows that office space is attracting the highest level of investor interest in England.

Research from BPS London shows that office space is currently the most in-demand commercial property asset class, with 30.5% of office opportunities either under offer or sold subject to contract. This indicates that businesses are shifting back to office-based working after the pandemic. Retail spaces are a close second with 30.2% of opportunities under offer, followed by industrial and warehouse opportunities at 27.5%. Meanwhile, investor demand is much weaker in the leisure and hospitality sectors, with only 16.1% of opportunities attracting an investor.

Investors are showing particularly strong interest in office spaces in the West Midlands (39.0%) and the South East (36.6%). London offices are attracting lower levels of interest (21.6%) – this is likely due to oversupply, with offices representing 71.0% of all available commercial rental stock in the capital.

Research from Knight Frank offers an insight into the current state of the London office market.

Office take-up in the capital reached 12.1 million sq. ft across 1,400 deals in 2025, marking London’s strongest performance since 2019. This was partly driven by a notable rise in demand for larger spaces, with around 70% of major corporate lettings in Central London expanding their office footprint last year.

However, supply of prime space is limited; vacancy rates for new, high-spec offices in the City Core are now at 0.3%. Competition is likely to intensify in the coming years, as up to 50 million sq. ft of London office leases are due to expire between now and 2030. Philip Hobley at Knight Frank commented, “London’s business sector’s growth urgently requires new supply to be unlocked in all of its key submarkets in order to meet structural demand over the next five years.

Analysis by the British Property Federation (BPF) shows that 81% of commercial buildings in major UK cities have an EPC rating below B.

The research analysed commercial buildings across all asset classes in London, Birmingham, Bristol, Leeds, Liverpool, Manchester and Newcastle. It found that only 3% of buildings have an EPC rating of A, while 16% are rated B. Manchester has the most energy-efficient buildings, with 22% of commercial properties rated A or B. London follows closely at 21%.

In 2021, the government launched a consultation into minimum energy efficiency standards for non-domestic buildings. It proposed a target of EPC C by 2027 and EPC B by 2030, however these measures are yet to be officially implemented. Rob Wall, Assistant Director at BPF, urged the government to take action, saying “Clarity on future standards is critical to increasing demand, attracting investment and building green skills and supply chains.”

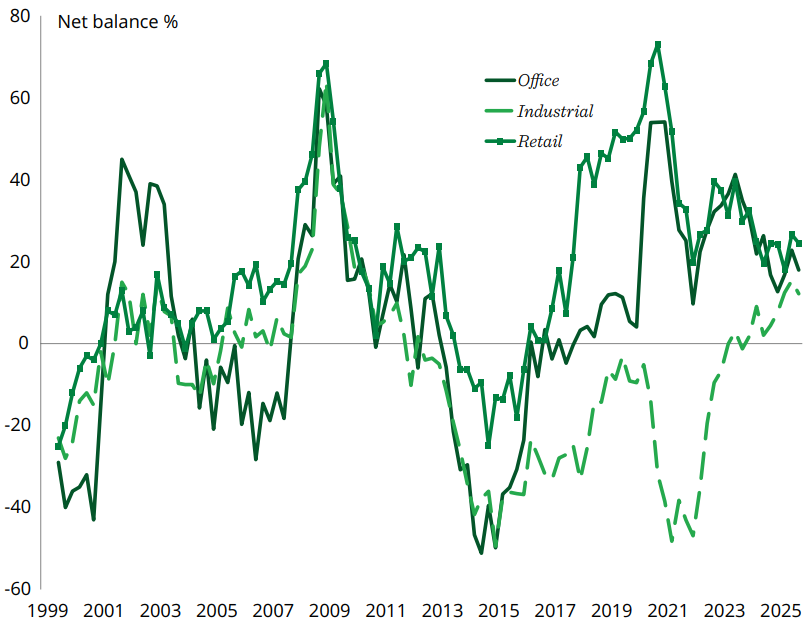

Occupier demand – broken down by sector

Availability – broken down by sector

All details are correct at the time of writing (18 February 2026)

Source: RICS, UK Commercial Property Monitor, Q4 2025