Our monthly property market review is intended to provide background to recent developments in property markets as well as to give an indication of how some key issues could impact in the future.

We are not responsible or authorised to provide advice on investment decisions concerning property, only for the provision of mortgage advice.

The latest UK Residential Survey from the Royal Institution of Chartered Surveyors (RICS) shows a loss of momentum in March.

The report indicates that buyer confidence has been knocked by world events, with new buyer enquiries declining to a net balance of -39%, down from -29% in February. This has filtered through to agreed sales, which dropped from -13% to -34% in March.

Higher borrowing costs have impacted the outlook for the coming months, with short-term expectations falling to -33%, a sharp drop from -4% in February.

The lettings market showed more resilience, but tenant demand continues to outweigh supply. As a result, near-term rental expectations increased to a net balance of +29%.

Tarrant Parsons at RICS commented, “What had been a cautiously improving picture for activity has been knocked off course by the wider macro fallout from the Middle East conflict, as the renewed deterioration in the mortgage rate outlook has proved particularly challenging.”

It was a relatively strong start to the year for prime property markets, but geopolitical uncertainty may dampen activity.

market activity was above the previous year’s level for the first time since last September; however, the £1m-plus segment was slightly lower. Savills notes that London, the South West and West of England showed the most resilience in Q1. However, prime values in the capital’s more domestic markets decreased by -0.5%, and price sensitivity is likely to persist.

Frances McDonald at Savills said, “For buyers who can see through the current disruption and take a medium-term view, properties at the top end remain good value, with prices not far off where they were pre-pandemic in many cases. But, with so much uncertainty about where things go from here and the financial markets so reactive, sellers will need to be realistic on pricing this spring.”

Looking to buy a family home this year? Rightmove has published the most affordable areas to settle down.

Overall, the report shows that buyers could look outside city centres to help their money go further, with coastal towns and market villages often more affordable. The top three most affordable towns to buy a family home are all in the North East - Shildon takes first place, where an average three-bed home costs £82,500. Towns in Wales and Scotland also featured on Rightmove’s list, but no Southern locations made it into the top ten, highlighting that the regional divide persists. However, there are still options for those looking to buy in southern regions. Rightmove recommends looking at more rural areas in the South West such as Cinderford, where a typical three-bed costs £272,250. Meanwhile, Dover is the most affordable option in the South East at £280,300.

Data from CBRE shows that capital values for UK commercial real estate held steady in Q1, while total returns were at 1.4%, driven by income returns.

In Q1, the retail sector recorded the highest total returns at 1.7%. In March, retail rental values rose by 0.3%, driven by a 1.0% increase in shopping centre rents. Meanwhile, office total returns were slightly more modest in Q1 at 0.9% and capital values fell by 0.1% in March due to a decline in outer London/M25 and central London offices.

The industrial sector recorded the highest month-on-month total returns in March (0.6%). It was therefore the second strongest sector in Q1, with quarterly returns of 1.6% and with all industrial segments showing consistent performance.

Steven Devaney at CBRE said, “We expect that income will remain the primary driver of performance through the rest of the year, with better performance anticipated from markets that have strong occupational fundamentals.”

The rateable values of non-domestic properties have recently been updated, so businesses may notice changes to their tax bill.

Every three years, the rateable value of non-domestic properties is updated, which local councils use to calculate Business Rates bills. The latest revaluation came into effect on 1 April 2026 and will run until March 2029.

A rateable value is based on the amount of rent that a property could have reasonably been let for on a certain date – in the latest revaluation, this date is 1 April 2024. The rateable value is not necessarily the actual amount of rent paid on that date, nor is it the same as the actual Business Rates bill.

Not all businesses will be affected in the same way - some will face higher bills and some will see reductions. Businesses are able to challenge valuations they believe are incorrect.

At the start of the decade, the retail sector was one of the weakest commercial asset classes due to the rise of online shopping. However, the sector is showing signs of strong recovery as it enters a new era.

Retailers have been forced to get creative and find new ways to bring consumers through their doors. Due to this, there has been a shift towards ‘experiential retail’ – where stores offer meaningful experiences that shoppers can’t get online. To achieve this, some shops now have interactive areas, cafes or product customisation to increase footfall. As a result, retail was the best performing property asset class in 2025, achieving a total return of 9.6% according to Knight Frank. Meanwhile, CBRE noted that vacancy rates decreased last year, with retail parks and central London streets being particularly popular areas. The improved sentiment is expected to continue in 2026, with CBRE forecasting annual retail sales growth of 1.9%.

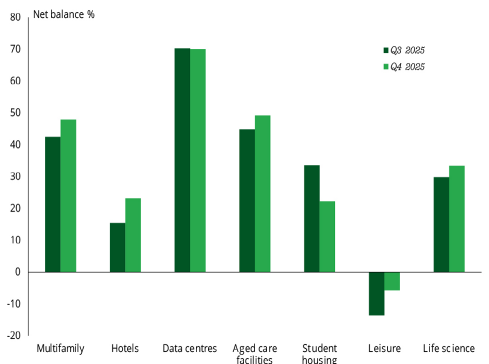

12-month capital value expectations – broken down by sector

– Prime commercial real estate capital value projections upgraded slightly for the year ahead

– In the retail sector, prime assets are anticipated to see capital values edge up by just 0.5%

– Prime office values are projected to rise by 1.9% (compared to 1% previously).

12-month rent expectations – broken down by sector

– Rental growth projections upgraded slightly for the year ahead

– Prime office rents are now anticipated to grow by 2.5% (up from 1.7% in Q3)

– Prime industrial sector rents are now rising by 2.1% (versus 1.6% pencilled in previously).

All details are correct at the time of writing (22 April 2026)

Source: RICS, UK Commercial Property Market Survey, Q4 2025